By Rob Whittet, Agency Partner | CO License #342852

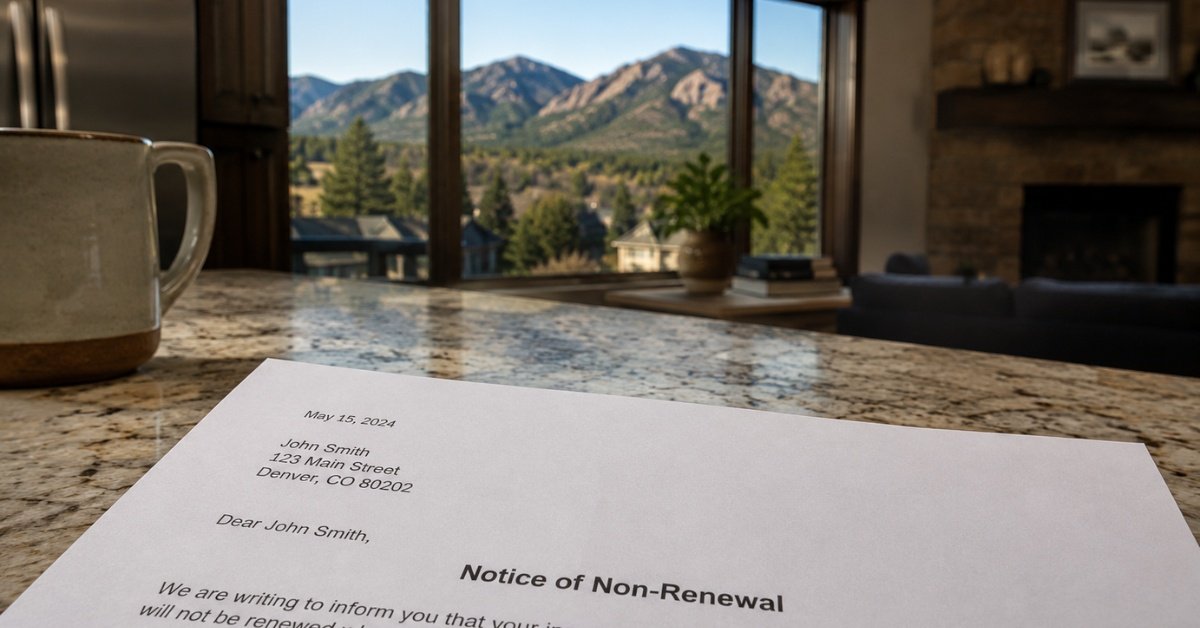

The letter arrives by mail, usually sixty to ninety days before your policy expires. It is a Notice of Non-Renewal, and for Colorado homeowners in foothill communities, mountain towns, and anywhere near the wildland-urban interface, it has become one of the most stressful pieces of correspondence a family receives. If your property sits in one of Colorado’s designated high fire risk zones, see what’s changed for foothill homeowners under the new mitigation disclosure law.

I have had this conversation with Colorado homeowners hundreds of times over the course of my career, and the first thing I tell every one of them is the same: your personal insurance options are not gone. The initial reaction is almost always the same: disbelief, then immediate anxiety about the mortgage. Because if you have a mortgage, insurance is not optional. Your lender will force-place coverage on your property within days of a lapse, and that forced-placed coverage will cost more than almost any voluntary policy while covering significantly less. The clock on your non-renewal notice is real.

“You have options. The market has changed, and not every carrier you call is going to help you — but an independent broker can often find coverage that a direct search will never surface.”

— Rob Whittet, Agency Partner

What a Non-Renewal Notice Actually Means

A non-renewal is not a cancellation. There is an important legal distinction in Colorado. A mid-term cancellation terminates coverage before the policy expires, and carriers can only cancel for specific reasons defined under Colorado law — non-payment of premium, material misrepresentation on the application. A non-renewal means your carrier has decided not to offer coverage for the next policy term when your current term ends. Different situations with different legal implications.

Carriers do not need a claim-related reason to non-renew. In the current Colorado market, the most common reasons are location-based wildfire risk scoring, proximity to wildland-urban interface zones, updated catastrophe modeling that reclassifies areas previously considered lower-risk, and broader carrier decisions to reduce overall Colorado homeowner exposure after years of significant underwriting losses.

Thousands of Colorado homeowners receive non-renewal notices each year with clean claims histories, well-maintained properties, and no individual fault. This is a market problem, not a personal one. The path forward is finding the right placement for your property in a market that has fundamentally shifted.

Your Four Coverage Options — Ranked by Quality

When a homeowner calls me after a non-renewal, the first step is assessing their placement options realistically. There are four categories. The goal is always to find the best available option in the highest category.

Colorado Homeowners Coverage Options When Non-Renewed: A Comparison

| Coverage Option | Priority | Cost | Coverage Quality | Guarantee Fund? |

|---|---|---|---|---|

| Admitted carrier | Best | Standard | Standard — up to full replacement cost | Yes — state guarantee fund applies |

| Surplus lines carrier | Good | Higher — often $7,000–$22,000+ for high-risk | Varies — review policy terms carefully | No — carrier financial rating matters more |

| Colorado FAIR Plan | Last resort only | Highest per dollar of coverage | Capped at $750,000 ACV — no personal property or liability | N/A — state-created program |

| Lender force-placed | Avoid | Highest — added to mortgage | Lender’s loan balance only — no personal coverage whatsoever | N/A |

Admitted carriers with appetite for high-risk properties. A shrinking but still-existing group of admitted carriers continues to write policies on properties in moderate wildfire risk zones, particularly when the property has meaningful mitigation features: a newer roof with Class A fire-rated materials, documented defensible space, fire-resistant venting, and a clean loss history. Not every admitted carrier has stopped writing Colorado homeowners insurance in wildfire zones — and an independent broker knows which ones remain open and what they need to see in a submission.

Non-admitted surplus lines carriers. When admitted carriers cannot help, surplus lines carriers step in. These insurers are legally authorized to write coverage in Colorado for risks the standard market declines. The Colorado Division of Insurance explicitly acknowledges in its homeowner insurance toolkit that surplus lines may be the only viable option for properties in high wildfire risk areas. Surplus lines policies cost more, deductibles may be higher, and the Colorado Insurance Guarantee Association fund does not apply — but for a homeowner who needs to maintain a mortgage, a surplus lines policy with genuine protection is far better than forced-placed lender coverage. A personal umbrella coverage policy can also be layered separately to extend liability protection beyond the base homeowners limits.

The Colorado FAIR Plan. Colorado launched its Fair Access to Insurance Requirements Plan in April 2025. It is the state’s insurer of last resort for homeowners who cannot find coverage in the admitted or surplus lines markets, after demonstrating denials from at least three private insurers. Coverage is capped at $750,000 for residential properties and provides actual cash value — not replacement cost. A home that would cost $900,000 to rebuild at current Colorado construction costs, receiving a $750,000 cash value cap, could leave a homeowner substantially underinsured after a total loss.

Forced-placed coverage from your lender. If coverage lapses entirely, your lender places insurance on the property to protect their financial interest — not yours. It covers the loan balance, not full replacement cost. No personal property coverage. No additional living expense coverage if you are displaced. No personal liability coverage, meaning you are exposed to any liability claim on your property during the gap. It costs more per dollar than any voluntary policy. Everything above this option is better.

When I submit a placement for a high-risk Colorado property, the submission package I build for underwriters includes a property inspection report, documentation of every mitigation improvement the homeowner has made, a clear explanation of construction type and age, the fire department response rating for the location, and the homeowner’s complete loss history in CLUE report format. How a property is presented to an underwriter matters as much as the property itself in a market where appetite is limited.

What HB25-1182 Means for Colorado Homeowners Right Now

Colorado passed House Bill 25-1182 in May 2025, with key provisions effective July 1, 2026 — giving homeowners new tools when carriers use wildfire risk scores to make coverage decisions.

Any carrier that uses a wildfire risk model to make an underwriting, pricing, or non-renewal decision must now disclose that risk score to you in writing, annually. If you do not know your wildfire risk score, request it from your current or prior carrier. They are legally required to provide it.

The law also requires carriers to incorporate documented mitigation work into their risk assessments. Defensible space, Class A fire-rated roofing, ember-resistant venting — these must factor into the risk score. If a carrier does not incorporate mitigation into its model at all, it must provide a discount to homeowners who document qualifying mitigation efforts.

If you believe your risk score does not accurately reflect your property or the mitigation you have completed, you have a right to appeal directly to the carrier. The carrier must acknowledge the appeal within ten calendar days and provide a written decision within thirty days.

Steps to Take the Day You Receive the Notice

Your Non-Renewal Action Plan

- Call an independent broker immediately – Not a captive agent who represents one company. An independent broker with access to admitted carriers, surplus lines carriers, and the excess and surplus market. Every day not spent working toward replacement coverage is a day of exposure.

- Document your mitigation before anyone inspects – Photographs with timestamps, receipts for roofing work, defensible space clearance records, wildfire mitigation assessments from a certified professional. This documentation is what HB25-1182 requires carriers to consider, and having it organized before an underwriter reviews your property directly affects placement outcomes.

- Request your wildfire risk score – You are entitled to it. Understanding what drove the non-renewal decision helps your broker know what to address in the submission. If the score contains errors or does not reflect documented mitigation, initiate the HB25-1182 appeal process simultaneously with the replacement carrier search.

- Notify your lender – If you have a mortgage, your lender needs to understand the timeline to avoid triggering a forced-place action prematurely. A lender who knows you are working with an independent broker has a different posture than one who discovers a coverage lapse after the fact.

Frequently Asked Questions

Can a carrier non-renew my Colorado home insurance without giving a reason?

Colorado law requires carriers to provide written notice of non-renewal before policy expiration, but carriers are not required to provide a specific reason for the non-renewal decision. Most carriers include a general explanation. Under HB25-1182, if the non-renewal was driven by a wildfire risk score, you can request that score and the basis for it.

How long do I have to find replacement coverage?

Colorado law requires a minimum of sixty days’ notice before a non-renewal takes effect for policies in force for sixty days or more. The expiration date on the notice is your hard deadline. Begin the replacement process the day the notice arrives, not at the sixty-day mark.

What happens to my personal liability coverage during a homeowners insurance gap?

A standard homeowners policy includes personal liability coverage that protects you if someone is injured on your property or you accidentally damage someone else’s property. That coverage disappears the moment your policy expires without replacement. If someone is injured on your property during a coverage gap, you are personally liable for all costs. This is one of the most overlooked consequences of a coverage lapse.

Is the Colorado FAIR Plan a good long-term solution?

No. The FAIR Plan serves a real purpose as a last resort — it prevents a forced-place situation for mortgaged homeowners who have no other options. But the $750,000 cap, actual cash value limitation, higher cost, and absence of standard endorsements make it a floor, not a destination. The goal for any homeowner on the FAIR Plan should be to document and complete mitigation work that improves their risk score enough to return to the private market.

What is the difference between actual cash value and replacement cost coverage?

Replacement cost coverage pays what it costs to rebuild or repair your home with materials of similar kind and quality at current prices. Actual cash value deducts depreciation from that cost. On a twenty-year-old roof, actual cash value after depreciation may be a fraction of what a new roof actually costs. This distinction is most significant after a total loss, where the difference can be tens or hundreds of thousands of dollars.

Will filing a claim before my non-renewal hurts my chances of finding replacement coverage?

A claim filed before the non-renewal will appear on your CLUE report, which replacement carriers review during underwriting. This does not mean you should forgo a legitimate claim, but the context matters. Your independent broker can advise on how a specific claim is likely to affect placement options given your current situation and the carriers being approached.

Licensed • Insured • 200+ 5-Star Google Reviews • 30+ Years Combined Experience