Home / Business Insurance / Commercial Umbrella Insurance

Commercial Umbrella Insurance for Colorado Businesses

By Rob Whittet, Agency Partner | CO License #342852

Commercial umbrella insurance provides an essential safety net for your Colorado business. When a catastrophic lawsuit or major accident exhausts the limits of your primary policies like general liability or commercial auto your umbrella coverage activates to pay the difference. Whether you run a small retail shop or a large construction firm, business umbrella insurance protects your assets, your earnings, and your future from a single unexpected verdict.

🛡️ No call centers. No spam. Just local experts.

⭐⭐⭐⭐⭐

5.0 Google Rating

Licensed & Insured

200+ 5-Star Google Reviews

30+ Years Combined Experience

Why Standard Liability Limits Are No Longer Enough

Running a business in Colorado means accepting a certain level of risk. While your standard Business Owner’s Policy or general liability coverage provides a strong foundation, the legal landscape has changed dramatically. We are currently in an era of social inflation, where juries are increasingly awarding massive settlements against businesses of every size.

According to the Swiss Re Institute’s sigma 4/2024 report on social inflation, litigation costs drove U.S. liability claims up by 57 percent over the decade ending in 2023, reaching an annual peak growth rate of 7 percent in 2023 alone. A separate study by Marathon Strategies found that thermonuclear awards exceeding $100 million are becoming more common, particularly in industries involving commercial vehicles and public premises.

If a customer suffers a severe injury on your premises, or your company vehicle is involved in a multi car accident on I 25, a $1 million commercial umbrella liability insurance limit can be exhausted rapidly by medical bills and legal defense costs alone. Without a business umbrella insurance policy in place, your assets, future earnings, and even personal property could be liquidated to satisfy the remaining judgment.

Ready to explore your options?

How Colorado's Higher Damage Caps Increase Your Business's Exposure

Colorado businesses now face larger potential liability verdicts than at any point in state history. Under House Bill 24-1472, signed into law in June 2024, the cap on noneconomic damages in Colorado civil lawsuits rose from $250,000 to $1.5 million for cases filed on or after January 1, 2025, and that ceiling adjusts upward for inflation every two years beginning in 2028. Noneconomic damages cover pain, suffering, and emotional distress, and they are awarded on top of economic damages like medical bills and lost income, which have never been capped. For a Denver-area business owner, this means a single serious injury lawsuit can now produce a far larger judgment than the same claim would have before 2025. When a verdict climbs into seven figures, a standard $1 million general liability limit is often exhausted long before the claim is paid in full. A commercial umbrella policy is what stands between that shortfall and your business assets.

How Business Umbrella Insurance Coverage Works in Colorado

Whether you call it a commercial umbrella policy or a business insurance umbrella policy, the mechanics are identical. An umbrella policy activates only after your underlying primary coverage has been completely exhausted. It acts as a financial safety net, extending the liability limits of several primary policies simultaneously.

For a detailed breakdown of what drives umbrella costs in Colorado and which businesses carry the highest exposure, read our commercial umbrella insurance guide.

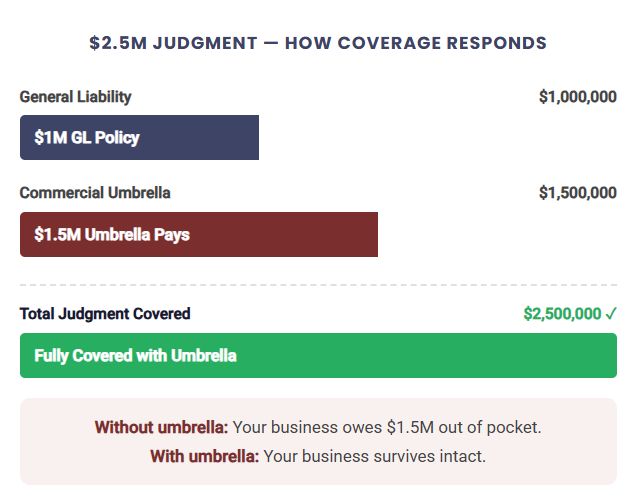

A Real World Example

Imagine your Centennial based contracting business carries a general liability policy with a $1 million limit. A severe accident at a job site results in a $2.5 million judgment against your company.

Your general liability policy pays the first $1 million.

Without an umbrella policy, your business owes the remaining $1.5 million out of pocket.

With a $2 million commercial umbrella insurance coverage policy, the umbrella pays the remaining $1.5 million and your business survives intact.

What Underlying Policies Does a Commercial Umbrella Extend?

A commercial and business umbrella insurance policy typically extends the liability limits of:

General Liability Insurance: covering third party bodily injury, property damage, and advertising injury claims.

Commercial Auto Insurance: covering severe accidents involving business owned vehicles or fleets.

Employer’s Liability (Part of Workers’ Compensation): covering lawsuits from employees claiming negligence led to their workplace injury.

Business Owners Policy: the bundled liability and property coverage many small Colorado businesses carry as their primary protection. An umbrella extends its liability limits, not its property limits.

Commercial Umbrella vs. Umbrella and Excess Liability Insurance

Some carriers use the terms “umbrella and excess liability insurance” or umbrella excess liability insurance interchangeably with commercial umbrella. While there are technical distinctions between a true umbrella policy and a standalone excess liability policy, most small and mid sized Colorado businesses purchase a commercial umbrella that functions as both. Your BIG broker will clarify which structure is right for your specific coverage stack.

Exclusions: What Commercial Umbrella Coverage Does Not Include

Commercial and business umbrella insurance coverage is broad, but it is not a catch all for every business risk. It extends liability limits only. It does not cover damage to your own property or replace specialized professional coverage.

Professional Errors and Negligence: Mistakes or bad advice in your professional services require a separate errors and omissions policy.

First Party Property Damage: Damage to your own building, equipment, or inventory from fire or theft is covered by commercial property insurance.

Cyber Liability: Data breaches and ransomware attacks require dedicated cyber liability coverage.

Employee Injuries: Medical bills and lost wages for injured workers are covered by the primary workers’ compensation policy, not the umbrella.

Colorado Industries That Need Umbrella Coverage the Most

Any business can face a catastrophic lawsuit, but certain industries in Colorado carry a significantly higher risk profile due to public exposure, heavy machinery, or fleet operations. Small business umbrella insurance is especially critical in these sectors.

Contractors and Construction

Colorado’s booming construction industry faces a high risk of severe job site accidents, heavy equipment operation, and subcontractor liability claims. A single structural failure or worker injury lawsuit can far exceed a standard general liability limit. Business umbrella liability insurance is considered essential coverage for any Colorado contractor. Learn more about coverage built specifically for the trades on our contractors insurance page.

Restaurants and Hospitality

High foot traffic, liquor liability exposure, and the risk of widespread foodborne illness claims make restaurants and hospitality businesses among the most vulnerable to large jury awards. Umbrella liability insurance for small businesses in this sector is a critical financial safeguard. Learn more about coverage built for food service operators on our restaurant insurance page.

Manufacturing and Distribution

Product liability risks and heavy reliance on commercial trucking fleets create compounding exposure for Colorado manufacturers. A single defective product claim or fleet accident can generate multi million dollar judgments that exhaust standard policy limits.

Real Estate and Property Management

Premises liability for large apartment complexes or commercial buildings creates significant exposure when multiple injuries could occur simultaneously. Commercial umbrella insurance coverage provides the high limits that property managers need to operate with confidence.

Not sure if your industry requires umbrella coverage?

When Colorado Contracts Require Umbrella Coverage

On many Colorado construction projects, umbrella coverage is not optional. General contractors and project owners routinely require subcontractors to carry a set amount of umbrella or excess liability, often $1 million to $5 million, as a condition written into the subcontract and verified on the certificate of insurance before work can begin. If your umbrella limit falls short of what the contract demands, you can be removed from the project or held in breach. A licensed Colorado broker can confirm your limits satisfy each contract’s requirements before you sign.

What Does Commercial Umbrella Insurance Cost in Colorado?

Commercial umbrella insurance is one of the most affordable forms of business coverage, because it only pays out after your underlying policy limits are exhausted. According to claims data published by Insureon, small businesses pay an average of about $86 per month, and more than half pay $100 per month or less, though premiums range widely from roughly $400 to over $7,000 per year depending on risk. Your actual premium is driven by a handful of factors: the amount of umbrella coverage you buy, your industry and its lawsuit exposure, your annual revenue, the size of your vehicle fleet, and your claims history. A contractor running heavy equipment on Denver-area job sites will pay more than a Centennial accounting firm for the same limit, because the underlying risk is different. Because pricing is built off your specific exposure, the most reliable way to know your cost is a quote from a licensed Colorado broker who can structure the umbrella to sit correctly above your existing general liability, commercial auto, and workers compensation policies.

Want an exact number for your business?

Frequently Asked Questions About Commercial and Business Umbrella Insurance

Commercial umbrella insurance is a supplementary policy that provides an additional layer of liability protection above the limits of your primary business insurance policies, such as general liability or commercial auto.

There is no meaningful difference between commercial umbrella insurance and business umbrella insurance. Both terms describe the same type of policy: a supplementary liability policy that activates after your primary coverage limits are exhausted. The terminology varies by carrier and region, but the coverage is functionally identical.

Most small businesses in Colorado should carry a minimum of $1 million in commercial umbrella insurance, though businesses with significant assets, fleets, or high foot traffic often require $2 million to $5 million in coverage. A licensed BIG broker can review your specific risk profile and recommend the appropriate limit.

No, commercial umbrella insurance does not cover professional errors or negligence. You need a separate Professional Liability or Errors and Omissions policy to cover mistakes in professional services. A commercial umbrella only extends the limits of liability policies, not professional indemnity coverage.

Commercial umbrella insurance is generally one of the most affordable forms of business coverage, because it only pays out after your primary policy limits are exhausted. The exact premium depends on how much umbrella coverage you buy, your industry and lawsuit exposure, your annual revenue, and your claims history. A licensed BIG broker can review your underlying policies and provide a precise quote for the limit your business needs.

Umbrella and excess liability insurance both provide coverage above the limits of primary policies, but they work differently. A commercial umbrella policy can fill gaps across multiple underlying policies and may cover some claims not included in primary coverage. An excess liability policy strictly follows the terms of one specific underlying policy. Most small and mid sized Colorado businesses purchase a commercial umbrella, which provides broader protection.

Colorado law does not require most businesses to carry commercial umbrella insurance. However, umbrella coverage is frequently required by contract. General contractors, commercial landlords, and project owners in Colorado often require businesses to carry $1 million to $5 million in combined liability limits before they will sign a lease or award a job, and an umbrella policy is how most small and mid-sized businesses meet that threshold. Your BIG broker can confirm whether a specific contract requires umbrella coverage.

Ready to Protect Your Colorado Business?

A single lawsuit should not erase years of hard work. Our licensed Colorado brokers will review your current liability limits and help you secure affordable commercial and business umbrella insurance that closes your coverage gaps. We work with top rated carriers to find you the best policy at the most competitive price.

🔒 Your information is secure and never shared.